A.Panorska, Computational Statistics and Stochastic Modeling, Wroclaw University of Technology,, February 21, 2011 [

R.Weron, ISBIS-2008 International Symposium on Business and Industrial Statistics, Invited Session 2j "Quantitative Finance in High Frequency and Low Temperature", Prague, July 1-4, 2008 [

R.Weron, II Ogólnopolska Konferencja "Polska Elektroenergetyka - Realia, Problemy, Dylematy", Panel "Bezpieczeństwo elektroenergetyczne Polski", Warszawa, 28 maja 2008 [

R.Weron, 7th Annual International Conference 'Forecasting Financial Markets and Economic Decision-Making' - FindEcon'2008, Łódź, May 14-17, 2008 [

A.Weron, M.Magdziarz, Modelling anomalous diffusion and relaxation. From single molecules to the flight of the albatross. ,Jerusalem, 28.03.2008[

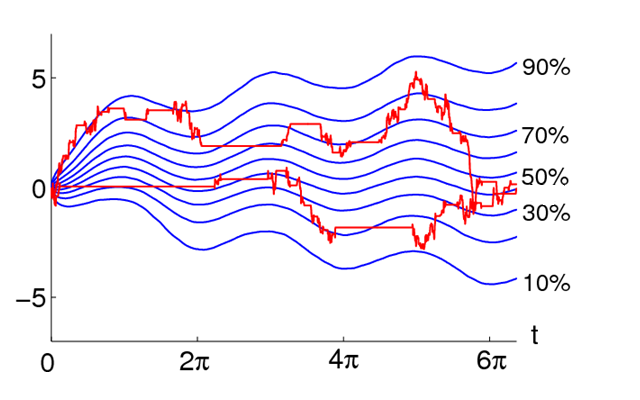

A.Wyłomańska, J.Nowicka-Zagrajek, 3 Ogólnopolskie Sympozjum "Fizyka w Ekonomii i Naukach Społecznych" FENS 2007,Wrocław, listopad 2007[

R.Weron, IGSSE Workshop on Energy: Modelling and Pricing, Munich, November 26-27, 2007 [

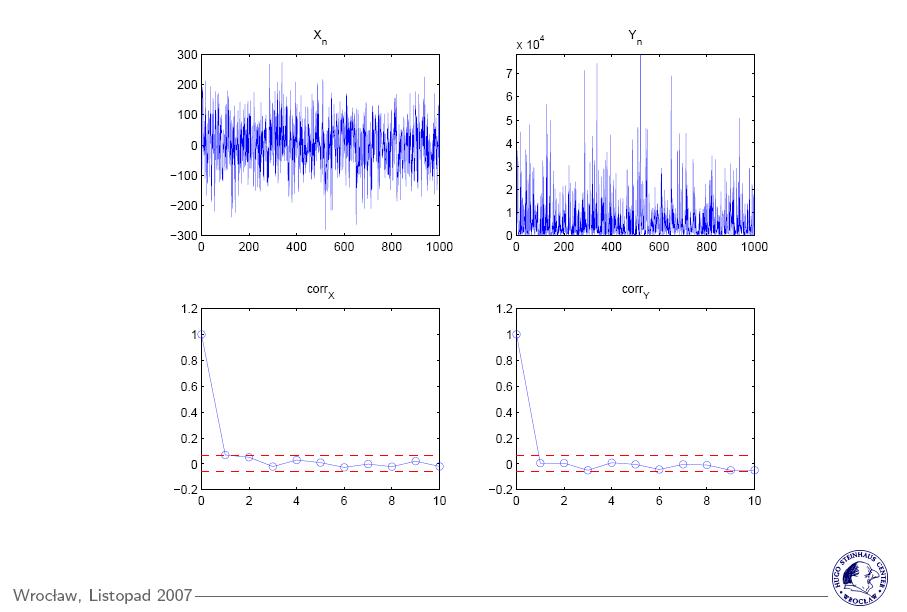

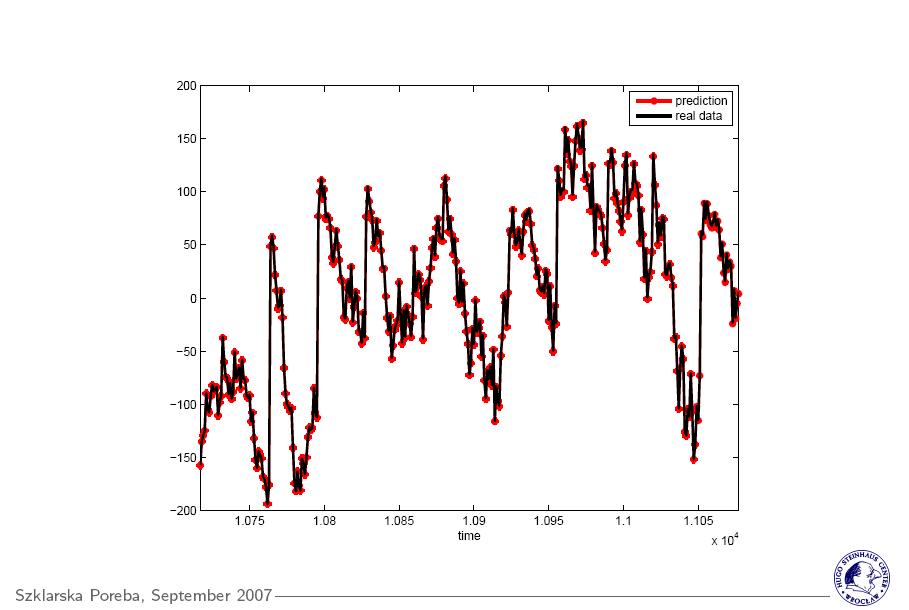

A.Wyłomańska,Konferencja Inwest 2007, Szklarska Poręba, Wrzesień 2007[

S,Truck, R.Weron, R.Wolff,56th Session of the International Statistical Institute, Invited Paper Meeting IPM71 "Statistics of risk aversion", Lisbon, Aug. 22-29, 2007 [

R.Weron,, Energyforum conference"Modelling & Measuring Energy Risk", Lisbon, June 14-15, 2007 [

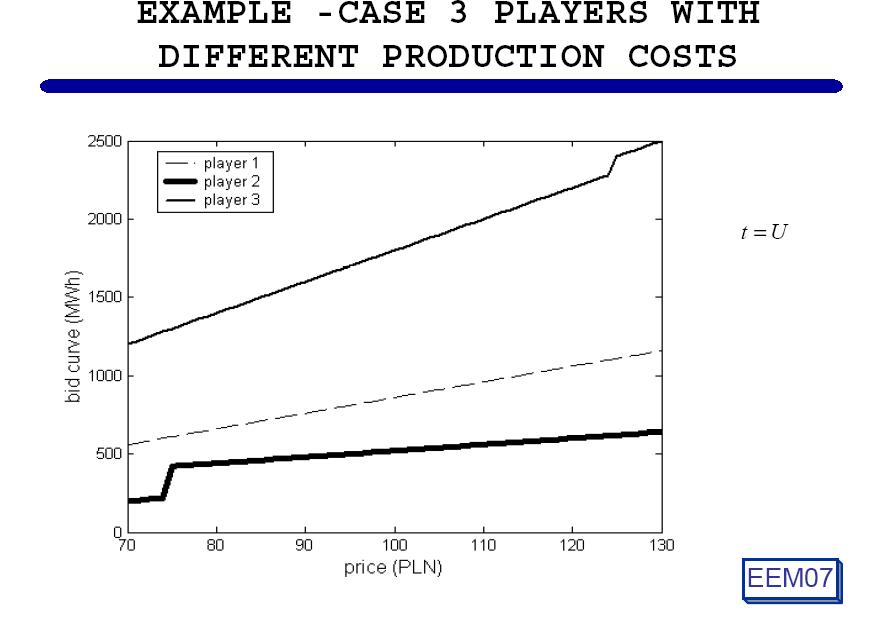

A.Wyłomańska, M.Borgosz-Koczwara, International Conference "The European Electricity Market EEM-07" , Krakow, May 2007[

R.Weron, Sz.Borak, 2nd AMaMeF Conference "Advances in Mathematics of Finance", Będlewo, Apr. 30 - May 5, 2007 [

|

"Point

and Interval Forecasting of Spot Electricity Prices:

Linear vs. Non-Linear Time Series Models" R.Weron, , DIME WP 2.4 Workshop "Instituting the Market Process: Innovation, Market Architectures and Market Dynamics", Manchester, Dec. 7-8, 2006 [ |

|

"Risk

management for energy companies" R.Weron, Modern Electric Power Systems MEPS'06, Wrocław, Sept. 6-8, 2006 [ |

|

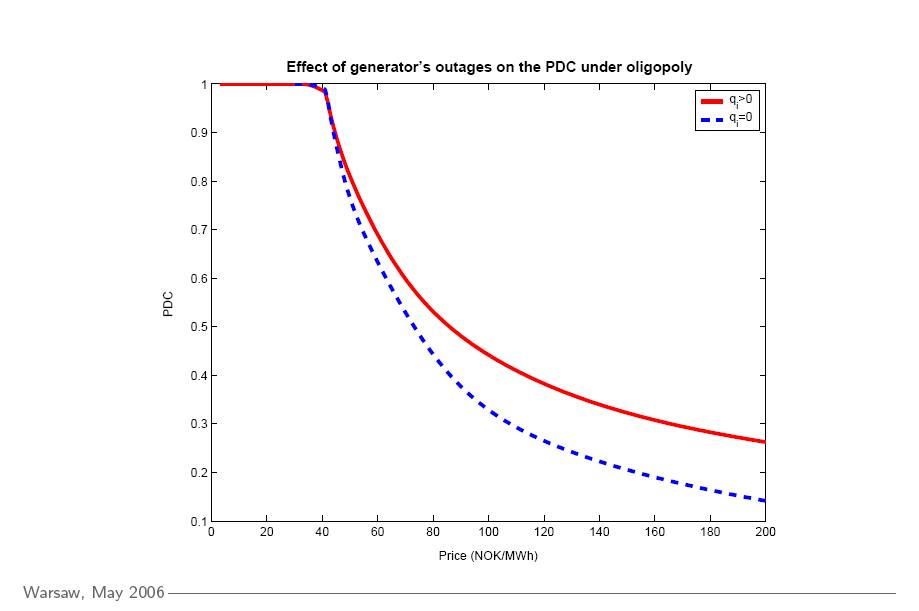

"A probability model for the electricity price duration curve"

A.Wyłomańska, M.Borgosz-Koczwara,International Conference "The European Electricity Market EEM-06", Warsaw, May 2006[ |

|

"Metody inżynierii finansowej w ubezpieczeniach"

J.Iwanik,PhD presentation [ |

|

"Visualization

tools for insurance risk processes" K.Burnecki, R.Weron, , Workshop on Data and Information Visualization, Berlin, Aug. 23-25, 2006 [ |

|

"Zarządzanie

ryzykiem. Część I: Narzędzia" R.Weron, "Psychologia Biznesu" (WSPiZ im. L. Koźmińskiego), Warszawa, 20 listopada 2005 [ |

|

"Heavy

tails and electricity prices" R.Weron,The Deutsche Bundesbank's 2005 Annual Fall Conference, Eltville, Nov. 10-12, 2005 [ |

|

"Forecasting

spot electricity prices with time series models" R.Weron, A.Misiorek,The European Electricity Market EEM-05, Łódź, May 10-12, 2005[ |

|

"Modelowanie

i prognozowanie zapotrzebowania oraz cen energii

elektrycznej w warunkach rynkowych" R.Weron,Seminarium Wydziału Elektrycznego Politechniki Wrocławskiej, Wrocław, 6 grudnia 2004 [ |

|

"Stochastic

volatility model of Heston and the smile" R.Weron,The Third Nikkei Econophysics Symposium, Tokyo, Nov. 9-11, 2004 [ |

|

"Pricing

derivatives in electricity markets" R.Weron,StochFin 2004 International Conference, Lisbon, Sept. 26-30, 2004 [ |

|

"Modeling

and forecasting electricity loads: A comparison" R.Weron,The European Electricity Market EEM-04, Łódź, Sept. 20-22, 2004 [ |

|

"Ryzyko,

Czarne Poniedziałki i długie ogony" R.Weron,"Psychologia Biznesu" (WSPiZ im. L. KoĽmińskiego) , "Ciekawe Wykłady" (SGGW), Warszawa, 6-8 maja 2004 [ |

|

"Periodically

correlated processes" R.Weron,Hejnice Compact Seminar, Hejnice, Feb. 12-16, 2004 [ |

|

"Energy

price risk management ... from a three year

perspective" R.Weron,XVIII Max Born Symposium, Lądek Zdrój, Sept. 22-25, 2003 [ |

|

"Everything

you always wanted to know about the Levy-stable law, but

were afraid to ask"

R.Weron,The Second ISM/SOKENDAI ECONOMICS Meeting, Institute of Statistical Mathematics, Tokyo, Nov. 11, 2002 [ |